Centum’s Debt Trap: Analyzing Covenant Breaches and Liquidity Strains at the Subsidiary Level

The Hidden Debt Pressure: Is Centum’s Subsidiary Leverage Threatening Future Value Realization?

Beyond the Parent: Uncovering the Cost of Capital, Covenant Breaches, and Asset-Liability Mismatches at Centum’s Subsidiaries

While Centum Investment Company Plc’s leadership continues to trumpet the “Centum 5.0” value optimization strategy—highlighting parent-level deleveraging as a major success—a deeper look at the consolidated group results reveals a far more concerning story. For the savvy shareholder, the “parent” is a mirage. To understand the true risk profile of your investment, you must look “beyond the parent” into the balance sheets of the subsidiaries, where the real threats to your capital reside.

1. The Growing Debt Mirage

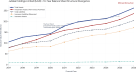

Investors have been led to believe that Centum is on a deleveraging path. However, the consolidated figures tell a different reality. As of 31 March 2025, the Group’s total debt stood at Ksh 17.85 billion, up from Ksh 16.59 billion the previous year.

While the parent company has reduced its direct borrowing (now at Ksh 440 million post-September 2025), the Group-level debt remains bloated and increasingly unsustainable. Based on the Group’s reported total equity of approximately Ksh 42.92 billion (as of September 2025) and total group borrowings of Ksh 17.85 billion, the Group’s Debt-to-Equity ratio sits at approximately 0.42. While this ratio may seem moderate in isolation, when combined with the specific high-cost, short-term nature of the subsidiary debt, it highlights a dangerous reliance on leverage to prop up long-term, illiquid projects. Far from shrinking, the Group’s consolidated debt obligations continue to exert massive pressure on the firm’s cash flow.

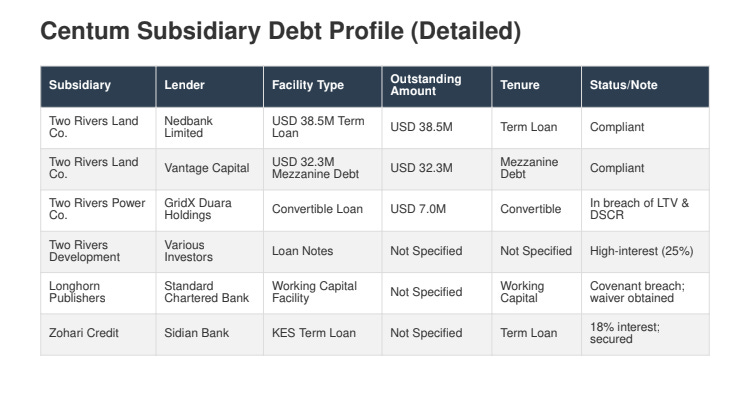

2. Detailed Subsidiary Debt Profile

The following table details key subsidiary debt facilities and their respective lenders, highlighting the concentration of risk outside the parent company:

3. Red Flags: Covenant Breaches and “Shylock” Rates

The most glaring red flag is the technical default occurring within the subsidiary portfolio:

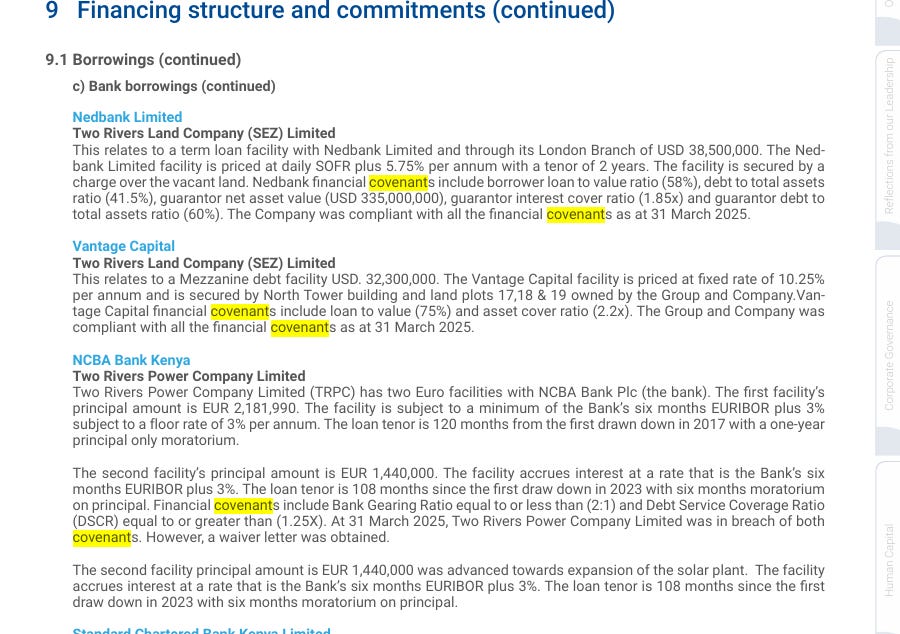

The Covenant Breach: Two Rivers Power Company (TRPC) has officially breached its Loan-to-Value (LTV) and Debt Service Coverage Ratio (DSCR) covenants. This is a “default event” that forced management to reclassify long-term debt as “current liabilities.”

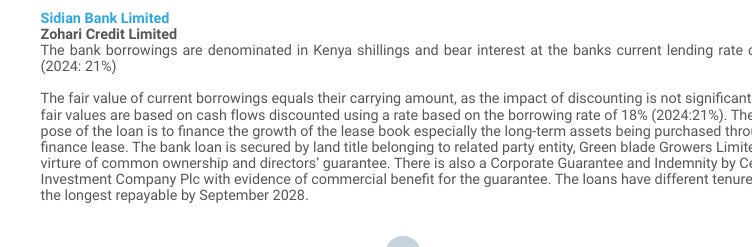

The Cost of Capital: Subsidiaries are operating under a crushing cost of capital. We are seeing interest rates as high as 25% on loan notes at Two Rivers Development. Even borrowing from Sidian Bank is at rates significantly higher than normal market lending, raising the question: Why is the cost of capital so punitive?

The Debt “Mismatch” and the Covenant Crisis

While the parent company’s headline figures suggest a deleveraging success story, a deep dive into the subsidiary-level financials reveals a hidden, growing risk: an alarming asset-liability mismatch. Centum is effectively using high-cost, short-term obligations to fund long-term, illiquid real estate and infrastructure projects. When those projects don’t exit (sell) on schedule, the cash flow crunch triggers a cascade of covenant breaches.

The Infrastructure Squeeze: The GridX Case

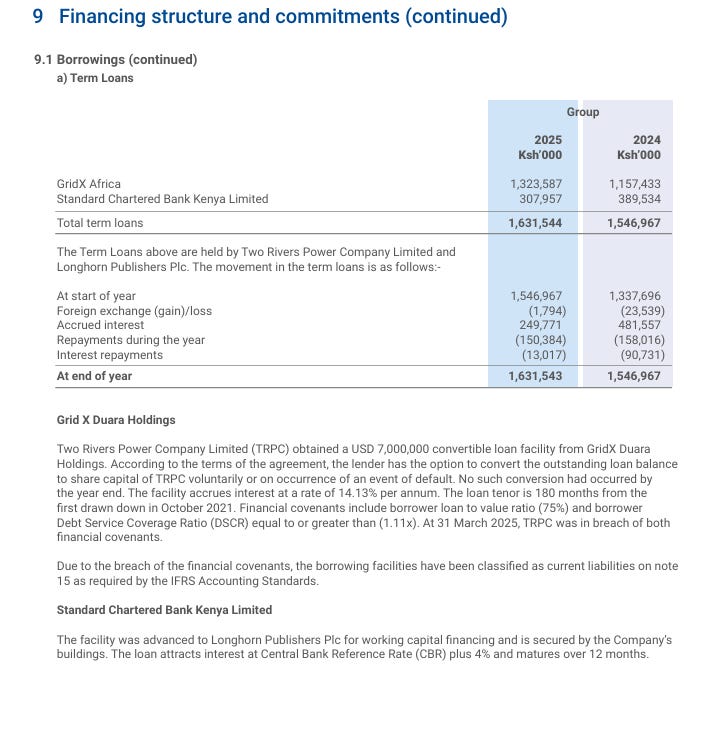

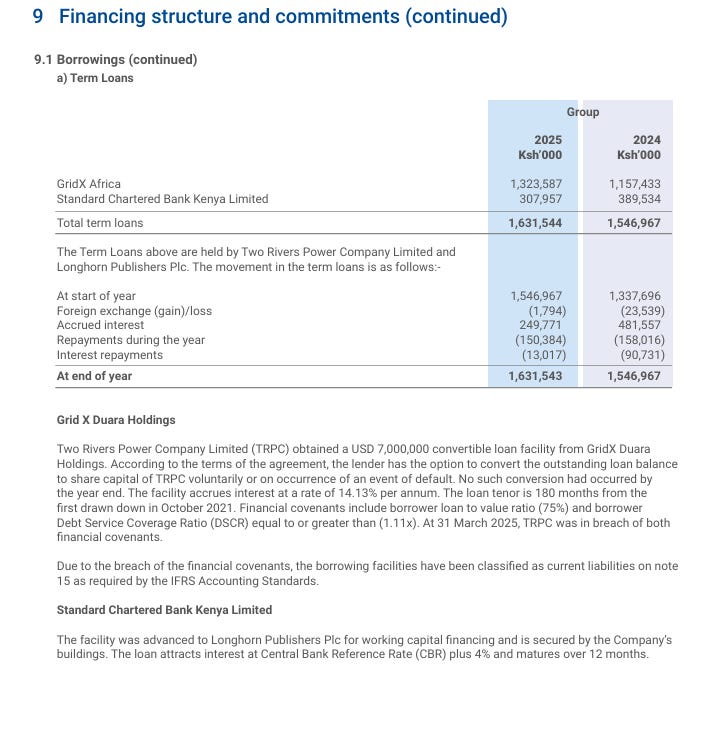

The most striking example of this pressure is the $7 million (approx. KSh 770M) convertible loan issued to Two Rivers Power Company (TRPC) by GridX Duara in 2021. Designed to fund essential solar and energy infrastructure, this facility was intended to make the Two Rivers development self-sufficient.

However, as of March 2025, the reality has diverged from the plan:

The Breach: TRPC tripped multiple financial “tripwires,” specifically breaching its Gearing Ratio and Debt Service Coverage Ratio (DSCR) covenants with both NCBA and GridX.

The Fallout: These breaches are not merely administrative; they are events of default. Lenders now technically hold the right to demand immediate repayment. Consequently, what were once long-term liabilities have been reclassified as “current liabilities” on the group’s balance sheet, creating an immediate liquidity overhang.

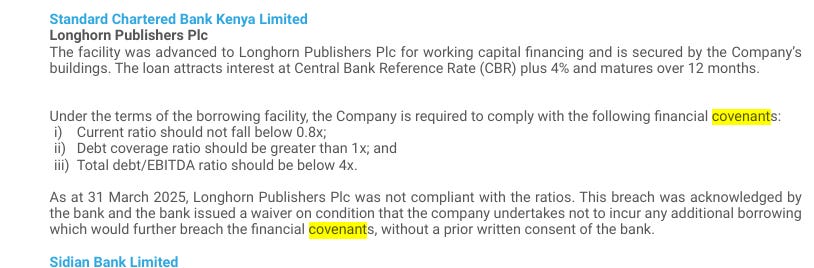

The “Leash” on Operations: The Longhorn Example

The situation at Longhorn Publishers mirrors this systemic vulnerability. After failing to meet its Current Ratio, Debt Coverage Ratio, and Total Debt/EBITDA covenants with Standard Chartered, the company secured a waiver—but at a high strategic cost.

Longhorn is now prohibited from taking on any new debt without the bank’s prior written consent. This “financial leash” restricts management’s ability to pivot or invest in growth, signaling that the bank—not the board—is effectively in control of the subsidiary’s balance sheet.

Why Shareholders Must Pay Attention

These aren’t isolated incidents; they are symptomatic of a broader strategy where subsidiary cash flow is failing to keep pace with debt service requirements.

Facility TypeRisk ProfileCurrent StatusBank DebtInterest Rate VolatilitySubject to floating rate hikes; requires waiversConvertible Debt (GridX)Equity Dilution RiskTechnical default; reclassified as current liabilityLoan Notes/ZohariHigh-Cost/Short-Term”Shylock-level” rates (16%–25% effective cost)

The Bottom Line: The Group’s “going concern” status is currently hanging on the successful monetization of assets like the TRIFIC REIT. If these exits do not close at the expected valuations, management loses its primary lever for deleveraging, and the liquidity trap will tighten. Shareholders should look for one thing in the upcoming results: tangible cash inflow from asset disposals, not just accounting-based portfolio valuations.

4. The Sidian Bank Exit: Forced Liquidity

The exit from the Sidian Bank holding is a revealing moment for shareholders. While officially framed as a strategic pivot, it carries all the hallmarks of a forced liquidation. Centum was unable to participate in the bank’s rights issue, effectively signaling a balance sheet stretched to the breaking point. When a parent company must offload a key, cash-generating asset because it cannot meet a capital call, it confirms that liquidity—not strategy—is currently driving boardroom decisions.

5. Management’s Mitigation Efforts

Management is currently operating in “triage mode” to stabilize the group:

Active Waiver Negotiations: Management is engaging directly with lenders to secure waivers for covenant breaches, aiming to avoid acceleration of debt repayments.

Asset Monetization: The core mitigation strategy is the “monetization” of assets. The planned sale of the TRIFIC North Tower to a USD-denominated REIT is intended to settle outstanding development facilities and unlock trapped capital.

Securing Third-Party Financing: Centum Real Estate is actively courting external financing lines to shift the debt burden away from the group balance sheet and onto project-specific entities with more manageable terms.

6. The Liquidity Trap: Asset-Liability Mismatches

The Group is currently caught in a classic financial trap: funding long-term, illiquid real estate and infrastructure projects with short-term, high-cost debt. This creates a distinct liquidity pressure where short-term debt obligations must be managed against long-term, illiquid development assets. The Group’s ability to monetize assets is now the only thing standing between the status quo and a potential liquidity crisis.

How expensive commercial paper debt is squeezing group cash flows

While the Holding Company has made headlines for its aggressive deleveraging, a look under the hood at the subsidiary level—specifically via Note 9.1b of the financial statements—reveals a more precarious reality. The Group is effectively operating in a “liquidity trap,” where expensive, short-term debt is cannibalizing the cash flow needed for long-term growth.

The High Cost of Unsecured Capital

The most glaring red flag is the cost of capital at the subsidiary level. Two Rivers Development Limited, the Group’s flagship real estate arm, has been carrying commercial paper debt at an eye-watering 25% interest rate.

For an unsecured instrument, 25% is rarely a sustainable long-term financing strategy. It reflects a high-risk premium that lenders demand when they lose confidence in traditional project cash flows. Instead of using cheaper bank debt or equity, these subsidiaries have been forced to bridge the gap between building costs and customer receipts using this high-cost “bridge” financing.

The Liquidity Squeeze

While the Group has successfully reduced its total outstanding commercial paper and loan notes from Ksh 2.12 billion in 2024 to Ksh 1.47 billion in 2025, this “success” comes at a hidden price:

Cash Allocation: Every shilling used to pay down this 25% debt is cash diverted away from new development opportunities or shareholder dividends. The Group is not necessarily “generating” wealth to pay these off; it is sacrificing its growth engine to kill off expensive debt that arguably should not have been used in such high volumes to begin with.

Operational Strain: Even Longhorn Publishers, which carries debt at a slightly lower 15% rate, is feeling the pinch. For a business with lower margins than a real estate developer, a 15% interest burden on short-term debt is a permanent anchor on the bottom line.

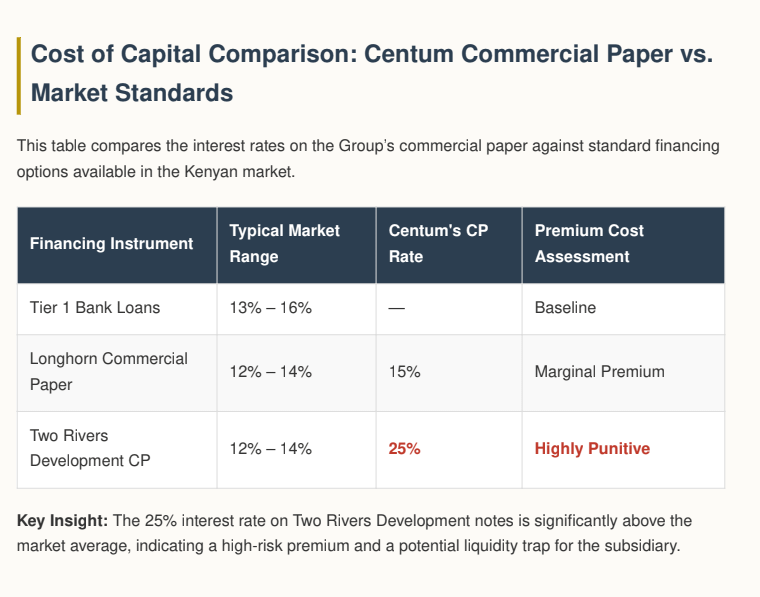

Cost of Capital Comparison: Commercial Paper vs. Market Standards

To visualize the “liquidity trap” described above, it is helpful to compare the interest rates on the Group’s commercial paper against standard financing options available in the Kenyan market. This table illustrates why relying on these short-term notes is a significant drag on profitability.

Key Takeaways from the Comparison

The 25% Threshold: The 25% rate on the Two Rivers Development notes is significantly above the market average for commercial paper. In a healthy company, commercial paper is used to lower the cost of borrowing by bypassing the banking intermediary. Here, Centum is doing the opposite—paying a “distress premium” that effectively erodes any margin the real estate project might otherwise generate.

The “Bridge” Penalty: Banks typically lend at the Central Bank Rate (CBR) plus a manageable margin. By opting for 25% commercial paper, the Group is paying nearly double the cost of standard bank debt. This suggests that the subsidiaries have either exhausted their traditional banking limits or are using these notes to bridge cash-flow gaps that banks are no longer willing to underwrite.

The Opportunity Cost: For every shilling of interest paid at the 25% rate, the Group is effectively losing the potential return that could have been earned if that capital were deployed into new business lines or high-yield assets.

The Strategic Outlook

The fact that these notes exist at 25% is a clear indicator that the subsidiaries are struggling with timing risk. They have long-term assets (buildings/land) that are not liquid, yet they are funding them with short-term, high-interest debt that demands immediate repayment. As an investor, the core concern is not just the debt itself, but the velocity of the cash flow required to pay it down before the interest burden becomes overwhelming

The Bottom Line for Investors

We are witnessing a classic case of capital misallocation. By relying on “shylock-level” commercial paper to fund long-term assets, the subsidiaries have created a cash-flow structure that requires constant, perfect execution of asset sales to avoid default.

If you are looking at Centum’s upcoming results, look past the debt reduction numbers. Ask whether the remaining debt is being retired through organic operational cash flow, or if the Group is simply “robbing Peter to pay Paul”—divesting productive assets just to service the interest on these expensive, short-term notes. Without a transition to lower-cost, long-term financing, the Group’s growth will remain effectively paralyzed by its own past borrowing decisions.

The “Pledge” Trap: Trading Future Value for Present Liquidity

One of the most concerning maneuvers in the Group’s recent financial history is the use of equity pledges—specifically the pledging of shares in subsidiaries—to secure financing for high-interest debt instruments like the Two Rivers Power Company (TRPC) facilities.

To the untrained eye, pledging shares might look like a standard corporate “security package.” In reality, when used to back expensive, high-interest obligations, it is a high-stakes gamble that signals a desperate liquidity position rather than a strategic financial maneuver.

Why Pledging Shares for High-Interest Debt is Rarely Prudent

In the world of project finance, infrastructure assets (like power plants) should ideally be financed through non-recourse project loans, where the cash flows from the asset itself are the primary security. However, when a company is forced to pledge the underlying equity of that project to secure “bridge” or high-interest financing, they are effectively trading their long-term future for short-term breathing room.

The “Margin Call” Risk: Pledging shares as collateral for debt carries the constant threat of a forced asset handover. If the subsidiary misses a covenant—like the Debt Service Coverage Ratio (DSCR) breach we’ve already observed at TRPC—the lender doesn’t just have a claim on cash; they have a claim on the ownership of the asset itself.

The Valuation Gap: Valuing equity in a private, development-stage project is inherently subjective. Lenders almost always apply a steep “haircut” to these pledges, meaning the Group has to tie up a massive amount of equity value to secure a relatively small amount of liquid capital. It is an incredibly inefficient use of the Group’s most valuable assets.

Loss of Strategic Autonomy: A subsidiary whose shares are pledged to a lender is, for all intents and purposes, a “zombie” entity. The lender will often place strict controls on dividend payments and operational spending to ensure they are first in line for any cash generated. Management effectively loses the ability to pivot the subsidiary or re-invest in growth, as every decision must first pass through the “filter” of the lender’s risk committee.

The Vicious Cycle of Over-Leverage

Using share pledges to manage 20%–25% interest debt creates a self-reinforcing downward spiral:

Distress Funding: The subsidiary is unable to access cheap bank loans due to poor performance, so it takes on high-interest commercial paper.

Collateralization: To appease lenders, it pledges its most valuable asset—the equity of the subsidiary—as collateral.

Dividend Lock: The lender restricts cash outflows to “protect” their collateral, preventing the parent company from seeing any return on its investment.

Forced Surrender: If the project fails to meet its targets, the lender exercises its right to the shares, and the parent company loses the asset entirely.

The Verdict for Investors

This is not “financial engineering”—it is a surrender. For Centum shareholders, this should be a major warning sign. If a project’s underlying cash flows were truly robust, they wouldn’t need to be backed by equity pledges for high-interest debt. When you see share pledges becoming a routine part of a subsidiary’s financing, it is a clear indicator that the Group is no longer managing growth—it is simply managing the pace at which it loses control over its own assets.

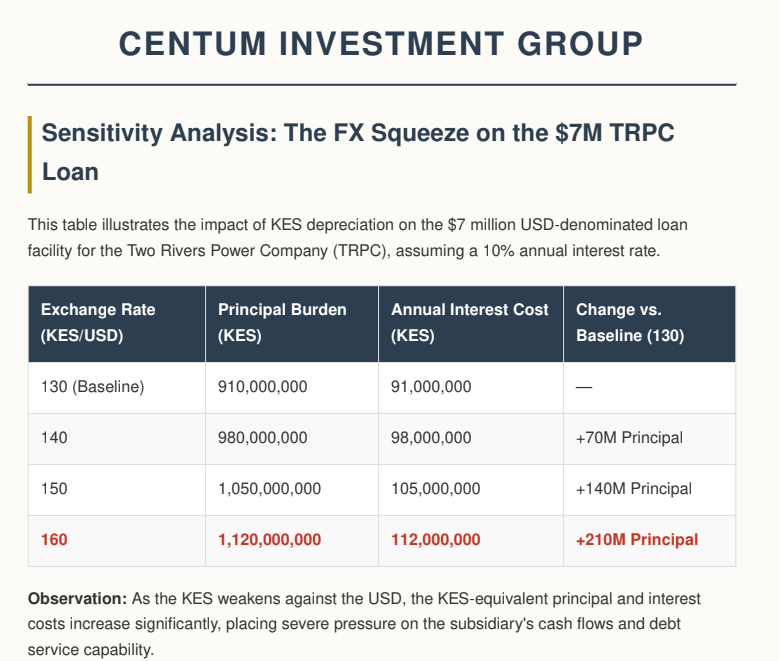

The FX Squeeze: The Invisible Debt Tax

Beyond the high-interest commercial paper, there is a more insidious risk lurking in the Group’s balance sheet: Currency Mismatch Risk. Centum’s infrastructure projects, such as the Two Rivers Power Company (TRPC), rely on USD-denominated debt (like the $7 million facility), while their revenue is generated primarily in Kenya Shillings (KES).

When the Shilling depreciates, this debt becomes a “silent” destroyer of shareholder value.

Sensitivity Analysis: The Cost of Devaluation

Assuming a 10% interest rate on the $7 million USD facility, the table below illustrates the impact of currency movement on the Group’s actual debt burden. This is not just a bookkeeping adjustment; it represents real cash flow that must be diverted from operations to service foreign-denominated debt.

The Structural Mismatch

The Principal Shock: If the Shilling weakens to 160 against the Dollar, the principal burden of this single loan balloons by KES 210 million. That is KES 210 million of equity value effectively “wiped out” by a currency move, even if the power plant’s operational performance remains perfectly steady.

The Interest Drag: The annual interest expense climbs by KES 21 million—a 23% increase. In an infrastructure project with fixed tariff structures, a sudden 23% spike in interest costs can trigger a Debt Service Coverage Ratio (DSCR) breach, forcing the subsidiary into a default scenario with its lenders.

The “Invisible” Tax: This represents an “invisible tax” on the parent company. While management might point to stable operational metrics, the hard-currency debt ensures that shareholders are effectively subsidizing the lender’s currency risk.

The Investor Verdict

This is a classic case of structural fragility. By mismatching “hard currency” debt with “soft currency” revenues, the Group has left itself vulnerable to macroeconomic shocks it cannot control.

Investors should look beyond the PLC’s debt-reduction headlines. The critical question for the next earnings cycle is: Do these subsidiaries have the pricing power to pass these currency-induced cost increases on to their customers? If the answer is no, then every slide in the Shilling is directly eroding the value of the underlying assets, turning manageable project debt into a noose that could eventually necessitate a forced sale of these assets to satisfy foreign creditors

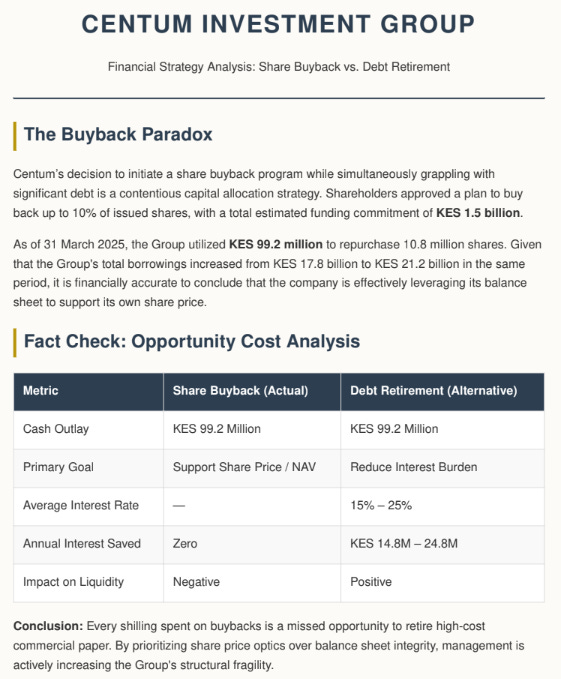

The “Share Buyback Paradox”: Borrowing to Buy Back Shares?

The most damning takeaway from Centum’s recent reports is the conflict between its capital allocation and its debt profile. While the Group has been vocal about its “deleveraging” strategy, the financial reality is that it has been spending cash on share buybacks while its total debt burden—and the cost of servicing that debt—has remained dangerously high.

The Numbers: What We Know

The Buyback Mandate: Shareholders approved a program to buy back up to 10% of the company’s issued shares. To achieve 100% of this plan (at the time of the announcement), the total funding commitment was estimated at approximately KES 1.5 billion.

Actual Spend: As of 31 March 2025, the Group has utilized KES 99.2 million to repurchase 10.8 million shares.

The Debt Reality: As of 30 September 2025, the Group’s “Borrowings” line item climbed from KES 17.8 billion to KES 21.2 billion.

Was Centum Borrowing to Buy Its Own Shares?

The short answer is functionally, yes. In corporate finance, cash is fungible. When a company holds KES 21.2 billion in debt—much of it at high interest rates—every shilling of internal cash flow belongs to the creditors until those debts are cleared. By choosing to allocate KES 99.2 million toward share buybacks rather than debt reduction, the company is effectively utilizing its remaining liquidity to “support” its stock price while leaving the debt burden to be refinanced or increased elsewhere.

The math is simple but harsh:

The Interest Bleed: The Group is paying interest rates of up to 25% on commercial paper.

The Buyback Drain: By spending nearly KES 100 million on buybacks, the Group is paying a “buyback penalty.” If that same KES 100 million had been used to pay down 25% interest debt, the company would have saved KES 25 million in interest expenses annually.

The Leverage Effect: Because the Group increased its total borrowings by over KES 3.4 billion in the six months between March and September 2025, the capital used for buybacks is essentially “borrowed” capital. The company is increasing its debt stack to fund returns to shareholders, a practice that is highly unusual and generally imprudent for a firm already struggling with liquidity.

Investor Takeaway for Your Substack

You are witnessing a company that is essentially “cannibalizing its own balance sheet.” > The Verdict: Management is attempting to engineer a higher Net Asset Value (NAV) per share by shrinking the denominator (the share count), but they are doing so using borrowed money. This is not organic value creation; it is a defensive maneuver to prop up the share price. By continuing this buyback program, the Group is choosing the appearance of value over the integrity of its balance sheet.

For your readers, the core question is clear: Why would a company borrow at 15%–25% to buy back shares that the market currently values at a massive discount? It suggests that even the company believes the “real” value is elsewhere, but they are trapped in an attempt to keep the stock price from falling further, even if it means weakening the company’s structural foundation to do it.

7. Investor Perspective

Shareholders need to stop looking at the parent’s debt reduction as a proxy for the Group’s health. Monitor the maturity profiles of subsidiary debt above all else. If you are a shareholder, the most critical number isn’t the “profit after tax”—it is the progress on asset monetization events. The Centum 5.0 strategy promises value, but until the subsidiary-level leverage is addressed, that value remains trapped under the weight of high-interest debt and operational dependency.

Disclaimer: This analysis is based on the FY2025 Integrated Report and HY2026 financial results. It is intended for informational purposes and does not constitute financial advice.

What stood out here is the distinction between parent-level deleveraging and the underlying economics at the subsidiary level. Debt maturity profiles, covenant compliance, and cash generation capacity often tell a very different story than headline leverage metrics and can ultimately determine strategic flexibility.

Quite eye opening.